“You Picked On the Wrong Guy”: How a Programmer Used AI to Expose His Insurer’s Overcharges (And Found $1,300 in Savings)

When his bill went up for no reason, Ben used AI to find out why - and ended up saving over $1,300 a year.

August 2, 2026 - Ben Thompson, a 34-year-old software engineer from Pennsylvania, was like most Americans: He’d been with the same car insurance company for years.

He paid his premiums on time. Never filed a claim. He assumed loyalty meant something.

It didn’t.

Last spring, Ben noticed his rate had crept up again - $89 more every six months.

No accident. No ticket. Just another “adjustment.”

That’s when Ben did something most people don’t: He decided to investigate.

Loyalty doesn't always pay

He spent an afternoon getting quotes from a series of different insurance companies—same coverage, same deductibles, everything identical.

What he discovered surprised him.

"I pretty quickly found a quote that was $1,300/year cheaper for the exact same coverage." Ben said.

"The issue is really that people don't have the time to compare prices for 50+ insurance companies. Nobody has that kind of time."

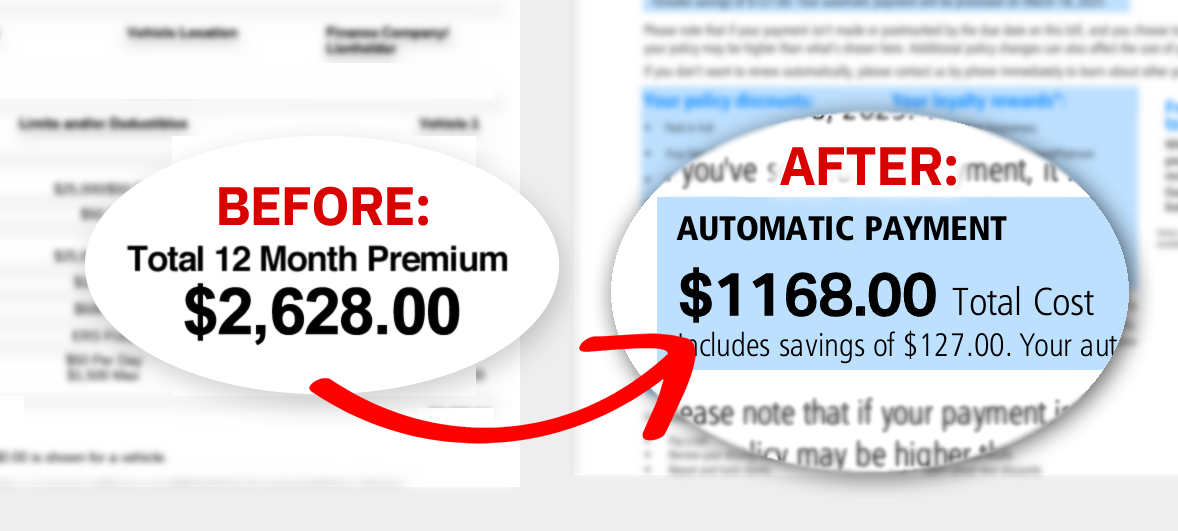

Here are Ben's actual bills, before and after:

How to Pay Less

Ben spent 3 months developing a site called StopOverpaying.org that uses AI to let you quickly compare different car insurance companies all at once.

You enter your information into a 2-minute form, and it outputs a series of insurance companies you can get quotes from.

Thousands Are Already Doing This

Since launching, StopOverpaying.org has helped over 100,000 drivers check their rates. According to ConsumerReports, the average driver who switches insurance saves $461 per year.

Some save more. Some save less. But most people discover one thing, they’ve been overpaying.

The process is:

✅ Free (no hidden fees, no credit card required)

✅ Fast (takes about 2 minutes)

✅ Private (no spam calls or texts)

Should You Check Your Rate?

If you’ve been with the same insurer for more than 12-18 months, the answer is almost certainly yes.

Even if you got a “good deal” when you first signed up, chances are your rate has quietly crept up – while better deals appeared elsewhere.

Here’s who should definitely check:

- You haven’t shopped around in 2+ years

- Your rate increased at renewal (even slightly)

- You’ve had no accidents or tickets

- You’re over 25 with a clean record

- You bundle home + auto (often overpriced)

Ben’s advice? “Just do it. Two minutes. I wish I’d done it years ago. I was literally throwing away over a thousand dollars a year for no reason.”

You are never locked into your current car insurance policy. If you have already paid your bill, you can cancel whenever you want. Some carriers will even cancel your old policy for you.

Here's how to do it:

- Step 1: Simply select your age below to look for discounts.

- Step 2: Enter your zip code and fill out the 2-minute quiz. You'll be given a list of companies to compare.