The 5 Stupidest Things Americans Overspend On (Hint: Coffee Isn’t One of Them).

By Ben F. | 02/27/2026

Advertiser Disclosure

Last updated July 17, 2025

I’m a massive coupon/savings nerd, and an embarrassing amount of my time is spent talking to people to find out how much they’re spending.

In my experience, the average American is overpaying for things on an almost daily basis.

Here are the worst culprits for overspending (and how you can save money by avoiding them):

1. Auto insurance.

Believe it or not, the average American family still overspends by $461/year¹ on car insurance.

Sometimes it’s even worse: I switched carriers last year and saved literally $1,300/year.

Here’s how to quickly see how much you’re being overcharged (takes maybe a couple of minutes):

Pull up StopOverpaying.org – it’s a free site that will compare offers for you

Answer the questions on the page

It’ll spit out a bunch of insurance options

That’s literally it. You’ll likely save yourself a bunch of money.

Here’s a link to StopOverpaying.org

2. Credit card debt (when some companies are willing to help pay it off for you).

If you’ve got $10k+ in unsecured debt (think credit cards, medical bills, etc), you could use a debt relief program and potentially save up to 45%.

Here’s how to quickly see if you qualify for debt relief:

Head to the National Debt Relief's site here

See what debt relief options are available

Find out if you qualify

Simple as that. You could end up paying less than you owed and be debt-free in 24-48 months. Here’s a link to National Debt Relief.

3. Stop getting price gouged when you shop online.

You might be surprised how often you’re overpaying on Amazon and elsewhere.

Big stores like Amazon know that no one has time to price shop through dozens of sites, so there’s often no incentive for them to offer bargain prices.

I typically hate browser extensions with a fiery passion, but if you don’t have Capital One Shopping installed yet, do yourself a favor and grab it.

When you shop online (on Amazon or elsewhere) it will:

Auto-apply coupon codes to potentially help save you money

Compare prices from other sellers to help make sure you’re not missing out on a better deal

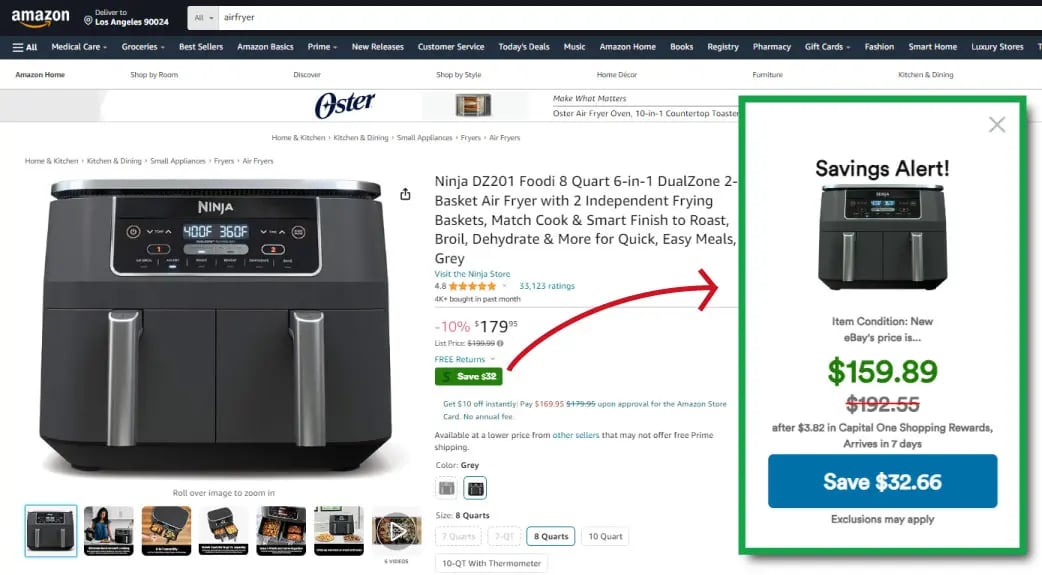

Here’s a quick example of how it works:

Savings will vary, this is just an example, of course.

Whenever the extension finds an available discount, you’ll see a little savings alert pop-up. For example, here you can save $32 on this air fryer.

Here’s a link to install Capital One Shopping, if you’re interested.

4. Not tapping into your home’s equity.

If you own your home but are low on funds, you might want to look into a HELOC (home equity line of credit). Instead of borrowing from your bank, you can essentially borrow from yourself (by tapping into your home's equity).

They may have lower interest rates and more flexible terms that a typical loan would.

Here’s a free page you can use to see how much you could access: link.

5. Home repair bills (let a company pay them for you instead).

Picture this: your trusty furnace suddenly throws a tantrum in the dead of winter, leaving you shivering and facing a repair bill that could cost you way more than you anticipated.

If you had a home warranty, you could be covered the next time something breaks down. It’s like having a safety net for your home (think plumbing, electrical, appliances, etc).

If you don’t have one yet, Choice Home Warranty is one of the bigger companies out there.

Bonus: home warranty companies usually have qualified, pre-vetted maintenance and repair workers ready to get the job done (which is one less thing to worry about).

If you’re interested just enter your zip code here to find a home warranty plan. It could save you a bunch of money the next time something breaks down.

6. Not getting a financial advisor.

Most people don’t have one, and it’s typically a huge mistake.

Sure, you can manage things on your own if you want to, but most people don’t have the time to actually do things right. There are huge benefits to having somebody pay attention to your money all the time.

People with financial advisors tend to beat the market by ~3%/year (according to a 2019 Vanguard Study). That can make a huge difference over time.

But more important: a good advisor will handle ALL of the annoying retirement stuff & bizarro tax implications you would have never thought of

If you don’t know a financial advisor personally, use a comparison site (like Datalign) and find somebody near you that has good reviews.

Or if you want something easier, here’s a quiz you can fill out that can find an advisor/planner based on your reqs.

7. Not using an adblocker.

If you aren’t using an ad blocker yet, I am begging you to try one. I am not exaggerating when I say it will change your life.

A good ad blocker will eliminate virtually all of the ads you’d see on the internet.

No more YouTube ads, no more banner ads, no more pop-up ads, etc. It’s incredible.

Most people I know use Total Adblock (link here) – it’s $2.42/month, but there are plenty of solid options.

Ads also typically take a while to load, so using an ad blocker reduces loading times (typically by 50% or more). They also block ad tracking pixels to protect your privacy, which is nice.

Here’s a link to Total Adblock, if you’re interested.

8. Overpaying on home insurance.

Switching home insurance will often save you more than switching auto policies (I’ve heard of people saving $1k per year by switching).

Here’s the home insurance comparison site I typically use: link.

9. Credit card interest payments.

High-interest credit card payments can be a nightmare. Have you ever wished you could just take a break from them?

You actually might be able to. Many people may not know, but there’s a great way to avoid interest payments for over a year or more.

It’s called a balance transfer. In simple terms, you move your balance to a new credit card that offers a 0% intro APR for a set period of time, which could help you save on interest.

If you’re interested, here are a few great balance transfer cards to look into: link here.

10. Paying for subscriptions you don’t even use.

We’ve all signed up for free trials and forgotten to cancel them. Stop paying for services you aren’t using!

Take a minute and get yourself a good cancellation app: I like Rocket Money (link here).

It’s an app that will put together a list of your subscriptions so you can pick/choose which ones to cancel.

They also have a premium service that will cancel them for you, if you’d like.

Here’s a link (it’s free).

11. Stop paying your credit card company.

If you’re stuck with credit card debt, you feel it. The high interest, the endless payments, the sinking feeling that you’re never getting ahead.

And let’s be honest—your credit card company isn’t on your side. It’s making a fortune off you with interest rates that can hit 36%.

So how do you get out of it? If you owe less than $100k, you can likely pay it off in one fell swoop using a debt consolidation loan.

Here’s how it works:

Use a site like AmOne to look at consolidation options (many loans offer far, far lower interest rates than your credit card company does)

Pick one that works for you

Use that loan to pay off your credit cards

Then, slowly pay off the debt consolidation loan over time

The upside: you’ll have just one monthly payment. And because personal loans typically come with lower rates (AmOne lenders offer options as low as 6.40% APR), you’ll get out of debt sooner. Plus, no credit card bill this month.

It takes less than 2 minutes to compare your options. No Social Security number required, just a real phone number (but don’t worry—they won’t spam you), and it won’t affect your credit score.

Here’s a link to AmOne’s site.

12. Missing out on $1,000+ a year because you weren’t in the loop.

The internet is huge, which means there are amazing money-making opportunities that pop up almost every day.

But most of them expire or sell out so fast that the public doesn’t have a chance to hear about them.

For example: back in September, there was a company offering $2,500/month for someone to literally watch shows on Netflix. Unsurprisingly, the role was filled so fast before most people knew it existed.

What if you could get access to great deals/money-making opportunities before other people do?

I spend every day looking for great ways to save/earn money, and whenever I find something really lucrative, I send out a text to our Betterbuck VIPs list first. (You can join it below, it’s 100% free)

It’s a great way to get tips about time-sensitive opportunities and deals before the rest of the country has time to hear about them.

You can join the list here:

That’s all (for now).

Those are my top savings tips for the time being, but I’ll keep adding to this article as I find new tips for you.

Thanks for reading!

StopOverpaying.org

- Compare car insurance rates fast

- Check multiple providers in minutes

- No spam calls